Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Everyone is waiting for the war to end, but is the oil price signaling a prolonged conflict?

Original Title: Oil Is the War

Original Author: Garrett

Translation: Peggy, BlockBeats

Editor's Note: While the market still considers oil price fluctuations as a "result variable" of war, this article argues that what truly needs to be understood is how war itself is being priced through oil.

With the continued blockage of the Strait of Hormuz, the global oil supply system is being forced to restructure — Asian buyers are massively turning to U.S. crude, WTI surpasses Brent, marking a structural shift in pricing mechanisms and trade flows. Short-term differentials can be explained by contracts, but at a deeper level, the question is "who can still supply."

The author further points out that the key misjudgment in the current market is not in price, but in time. The futures curve still implies a premise: that the conflict will end in the short term and supply will recover. However, the more likely path is a prolonged war of attrition. This means that the high oil price is no longer a temporary shock but will evolve into a more enduring structural state, with the range shifting or moving up to $120–150.

In this framework, crude oil is no longer just a commodity but has become the "upstream variable" of all assets. Its repricing will cascade through interest rates, exchange rates, stock markets, and credit markets.

The market has already priced in the onset of war, but has not yet priced in the continuation of war.

Below is the original text:

Trump gave Iran a 10-day deadline. That was already a week ago. Yesterday, he reminded everyone again: the countdown is now only 48 hours. Tehran's response was: no.

Five weeks ago, on February 28 when U.S. and Israeli warplanes struck Iran, the market's pricing logic was still that of a "surgical" airstrike: two weeks, at most three weeks; the Strait of Hormuz reopened; oil prices spiked and then fell back, all returning to normal.

But our judgment at that time was: no.

From day one, our core view was that this war would escalate first and only potentially cool down later. The most likely path was ground troop involvement, evolving into a long and protracted conflict. The downtime of the Strait of Hormuz would far exceed the assumption that the market was willing to incorporate into its models. We have provided a complete logic in terms of duration framework, Strait of Hormuz pricing model, and war variable analysis.

The core judgment is simple: Iran does not need to win, it just needs to raise the cost of war high enough to compel Washington to seek an exit strategy. And this "exit" will not accompany the smooth reopening of the strait.

Five weeks later, every key aspect of this assessment is being gradually validated. The Hormuz Strait has yet to reopen. Brent crude closed near $110. The Pentagon is preparing for weeks of ground operations. Trump's war aim has also shifted from "denuclearization" to "sending the other side back to the Stone Age," but he still cannot clearly define what "victory" means.

The deployment of ground troops is the escalation turning point we have been tracking. The Marine Corps and airborne units are already assembling in the theater of war, a moment that is now imminent.

But more crucial than the next round of airstrikes or the next ultimatum is oil.

Oil is not a byproduct of this war; oil itself is at the core of the war. The stock market, bond market, crypto market, the Fed, and even your daily food expenses — everything is a downstream variable. As long as the oil price judgment is correct, everything else will fall into place; once the judgment is wrong, all other decisions will become meaningless.

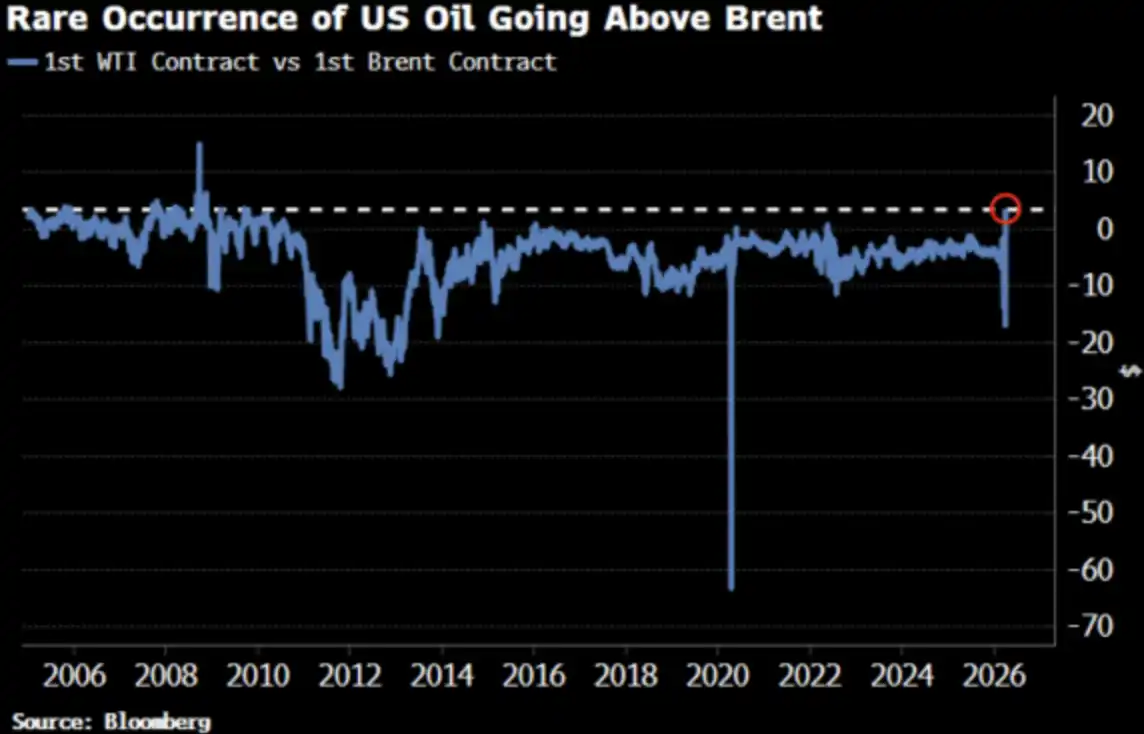

The WTI crude oil price has just surpassed Brent for the first time since 2022, a change that has already caught the market's attention.

Good, it should be this way.

WTI Surpasses Brent: Everyone Is Asking Why

On April 2, WTI crude closed at $111.54, while Brent closed at $109.03. WTI's premium over Brent was $2.51, the largest price difference since 2009. Just two weeks ago, WTI was at a significant discount to Brent.

Everyone is asking: What happened? Below is the summary version and a more realistic version.

Summary Version: Maturity Date Misalignment

The WTI front-month contract corresponds to May delivery, while Brent's front-month contract has rolled over to June. In such a tight supply situation, an "early one-month delivery" means a higher price — WTI just happened to have an earlier delivery date.

With 35 years of trading experience and currently working at Oxford, oil trader Adi Imsirovic stated that on top of historically high freight and insurance costs, buyers were willing to pay nearly $30 more per barrel for Brent crude delivered one month early. In his 35-year career, he has never seen such a situation.

This is a "mechanism-level" explanation — it is correct but not complete.

Real Version: Price Curve Is Overall Shifting

The convergence between WTI and Brent is not just a temporary misalignment of near-month contracts. Bloomberg points out that this phenomenon is clearly visible across multiple contract months, spanning the entire forward curve. In other words, the entire price curve is being repriced.

What is the reason? A shift in Asian demand. In late March, Asian refineries locked in about 10 million barrels of U.S. crude for May loading; the previous week, they also purchased about 8 million barrels. Kpler expects that U.S. crude oil exports to Asia in April will reach 1.7 million barrels per day, up from March's 1.3 million barrels per day. China, South Korea, Japan, and ExxonMobil's refinery in Singapore are all buying U.S. crude — because it is currently the "only game in town."

The Strait of Hormuz remains closed. Abu Dhabi's flagship crude Murban — the closest alternative to WTI — has disappeared from the global market. WTI is becoming the global "marginal pricing oil."

This is not panic buying but a structural shift in flows.

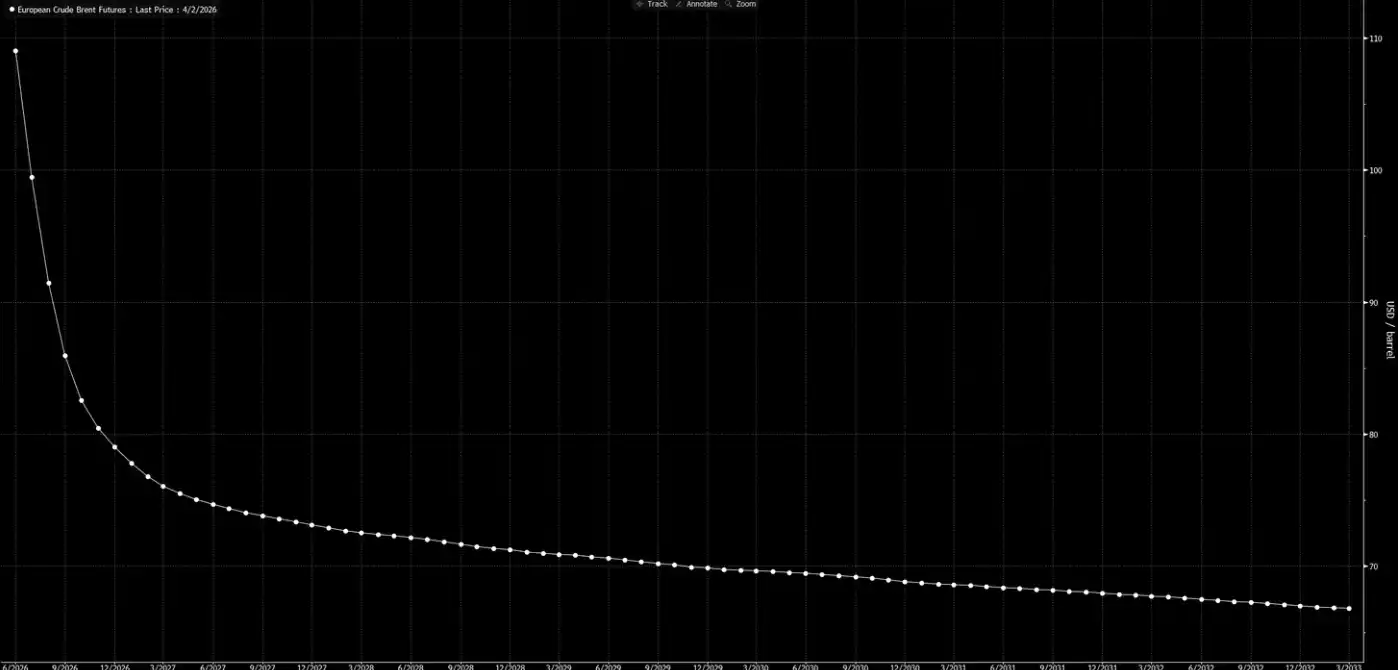

Now, let's look at the forward price curve again.

This curve is conveying a signal: this is just a temporary shock, and by Christmas, everything will be back to normal.

Our assessment is that this curve is "daydreaming."

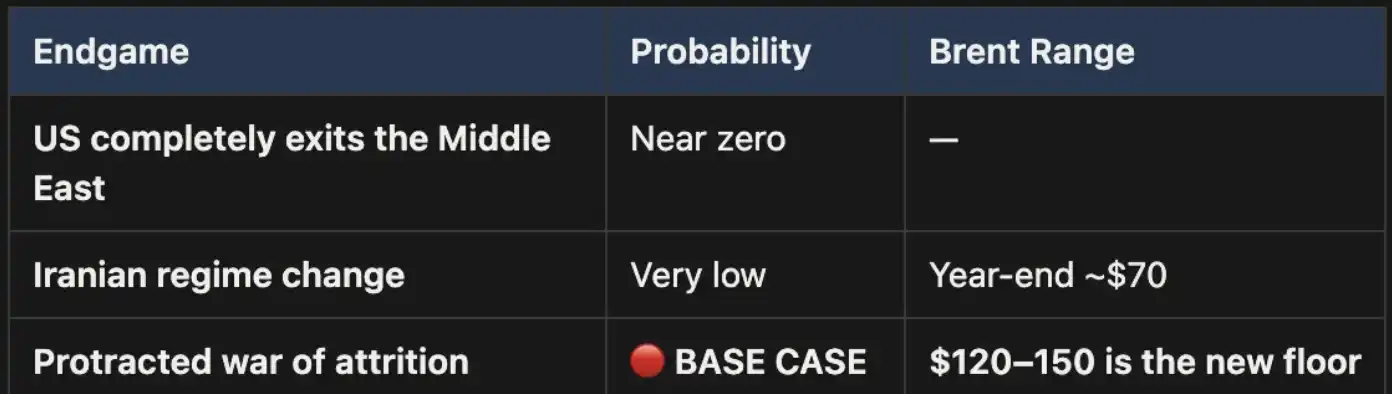

Three Endings, One Baseline Path

We have already presented this analytical framework in the "Weekly Signal Playbook." So far, there have been no changes; if anything, the probability of the baseline scenario has further strengthened.

This war will ultimately end in only three ways:

The three endings are listed in the graphic: one, complete U.S. withdrawal from the Middle East; two, regime change in Iran (similar to 2003 Iraq); three, a long-term attrition war.

Ending one is politically almost impossible.

Ending two also does not hold up: the terrain conditions, troop requirements, and the evolving logic of guerrilla warfare all indicate that this path is costly and hard to conclude. Iran's land area is three times that of Iraq, with a population almost twice as large, not to mention the mountainous terrain that would not offer invaders any respite. This is not 2003.

Ending three is the baseline scenario, and its probability is far ahead. If the conflict evolves into a long attrition war, the closure of the Strait of Hormuz will continue, and oil prices will remain high. This high level will be structural, not temporary. The current forward price curve clearly does not adequately price in this.

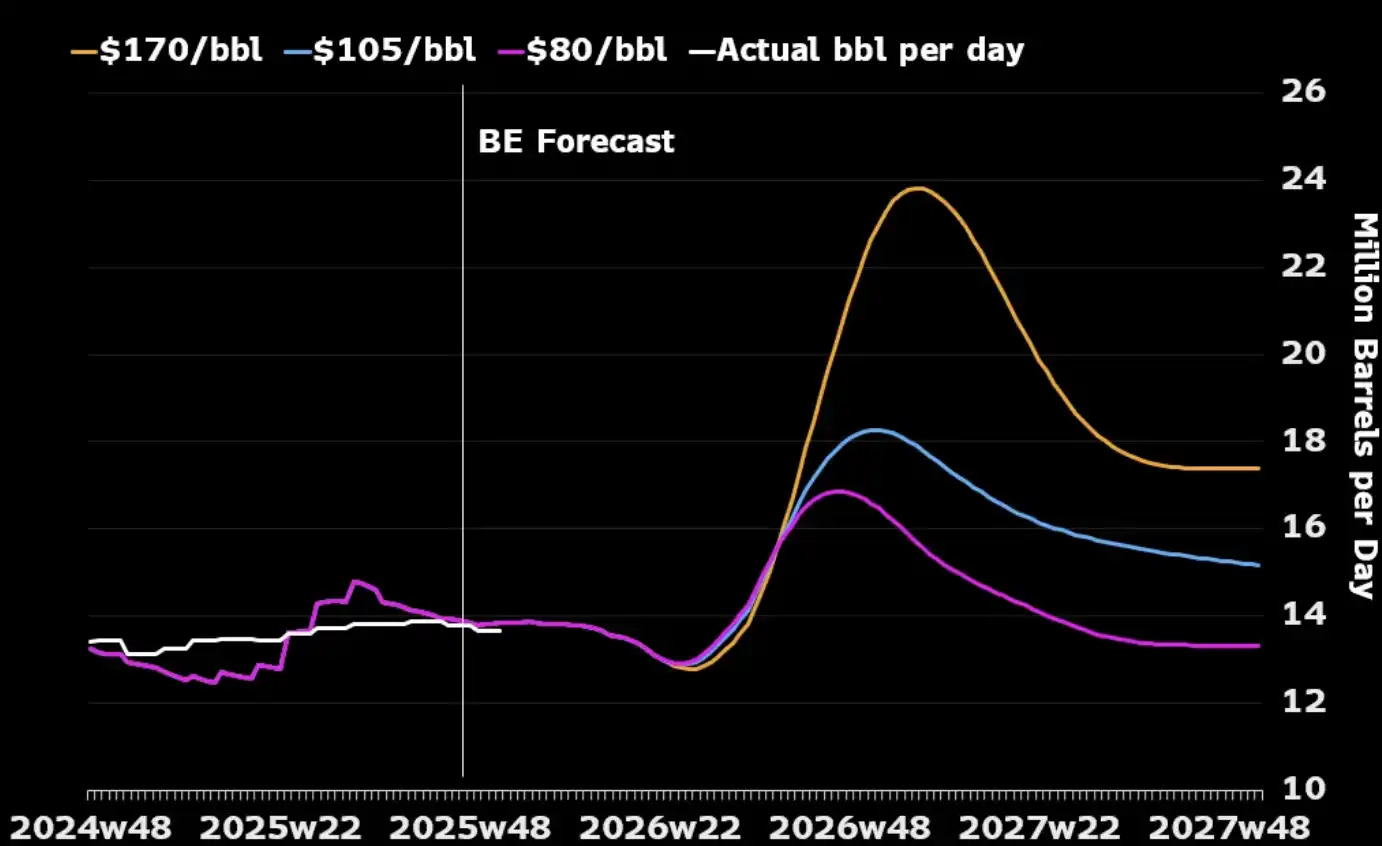

One often-overlooked point is this: looking solely at the oil industry itself, a prolonged war may actually align with U.S. strategic interests. The oil production capacity in the Middle East would be disrupted during the conflict, forcing global buyers to turn to North American energy as few alternative sources remain. The higher oil prices would also incentivize U.S. producers to expand output — increasing rigs and ramping up investment in shale oil. As shown in the graph below, almost every significant historical oil price spike has been followed by a U.S. production upturn within the subsequent 12 to 18 months.

The sole cost the U.S. truly needs to manage is domestic: how to prevent gasoline prices from persisting above $4 per gallon long term and sparking a political backlash. This is a "pain threshold" rather than a condition determining when the war ends.

Price "Arithmetic"

In a scenario where the Strait of Hormuz is closed, $110 Brent is not a ceiling but merely a starting point. In our base case, as long as the strait remains closed, oil prices will be maintained in the $120 to $150 range.

With each passing week, inventories are being depleted. UBS data shows that global inventories fell to the five-year average at the end of March — and that was before the latest escalation. Macquarie's assessment is that if the war drags on past 6 months and the strait remains closed, there is a 40% probability of oil spiking to $200.

The prompt spread (the price difference between the two most recent Brent contracts) has widened to $8.59/barrel. The market is paying around an 8% premium for "one-month forward delivery" — a level of tension not seen since 2008.

However, in 2008, there wasn't a physical blockage of 15% of global supply.

Today, nearly all models, price curves, and Wall Street year-end forecasts are based on the same assumption: that this conflict will end, the Strait of Hormuz will reopen, oil prices will return to normal, and the world will go back to how it was.

Our judgment is: it won't.

The back end of the forward curve has not caught up with reality. The market has already priced in "war happening" but has not yet priced in "war continuing." Every pullback in crude oil before the reopening of the Strait of Hormuz is an opportunity. This is our core position, and we are not hedged.

Oil is the first domino. When "boots on the ground" are deployed and there is no swift victory — when the conflict evolves into the enduring attrition we anticipated from day one — repricing will not stop at crude oil itself, but will transmit sequentially to interest rates, exchange rates, stock markets, and credit markets. This is what will happen next.

You may also like

ChainCatcher Hong Kong Themed Forum Highlights: Decoding the Growth Engine Under the Integration of Crypto Assets and Smart Economy

Why can this institution still grow by 150% when the scale of leading crypto VCs has shrunk significantly?

Anthropic's $1 trillion, compared to DeepSeek's $100 billion

Geopolitical Risk Persists, Is Bitcoin Becoming a Key Barometer?

Annualized 11.5%, Wall Street Buzzing: Is MicroStrategy's STRC Bitcoin's Savior or Destroyer?

An Obscure Open Source AI Tool Alerted on Kelp DAO's $292 million Bug 12 Days Ago

Mixin has launched USTD-margined perpetual contracts, bringing derivative trading into the chat scene.

The privacy-focused crypto wallet Mixin announced today the launch of its U-based perpetual contract (a derivative priced in USDT). Unlike traditional exchanges, Mixin has taken a new approach by "liberating" derivative trading from isolated matching engines and embedding it into the instant messaging environment.

Users can directly open positions within the app with leverage of up to 200x, while sharing positions, discussing strategies, and copy trading within private communities. Trading, social interaction, and asset management are integrated into the same interface.

Based on its non-custodial architecture, Mixin has eliminated friction from the traditional onboarding process, allowing users to participate in perpetual contract trading without identity verification.

The trading process has been streamlined into five steps:

· Choose the trading asset

· Select long or short

· Input position size and leverage

· Confirm order details

· Confirm and open the position

The interface provides real-time visualization of price, position, and profit and loss (PnL), allowing users to complete trades without switching between multiple modules.

Mixin has directly integrated social features into the derivative trading environment. Users can create private trading communities and interact around real-time positions:

· End-to-end encrypted private groups supporting up to 1024 members

· End-to-end encrypted voice communication

· One-click position sharing

· One-click trade copying

On the execution side, Mixin aggregates liquidity from multiple sources and accesses decentralized protocol and external market liquidity through a unified trading interface.

By combining social interaction with trade execution, Mixin enables users to collaborate, share, and execute trading strategies instantly within the same environment.

Mixin has also introduced a referral incentive system based on trading behavior:

· Users can join with an invite code

· Up to 60% of trading fees as referral rewards

· Incentive mechanism designed for long-term, sustainable earnings

This model aims to drive user-driven network expansion and organic growth.

Mixin's derivative transactions are built on top of its existing self-custody wallet infrastructure, with core features including:

· Separation of transaction account and asset storage

· User full control over assets

· Platform does not custody user funds

· Built-in privacy mechanisms to reduce data exposure

The system aims to strike a balance between transaction efficiency, asset security, and privacy protection.

Against the background of perpetual contracts becoming a mainstream trading tool, Mixin is exploring a different development direction by lowering barriers, enhancing social and privacy attributes.

The platform does not only view transactions as execution actions but positions them as a networked activity: transactions have social attributes, strategies can be shared, and relationships between individuals also become part of the financial system.

Mixin's design is based on a user-initiated, user-controlled model. The platform neither custodies assets nor executes transactions on behalf of users.

This model aligns with a statement issued by the U.S. Securities and Exchange Commission (SEC) on April 13, 2026, titled "Staff Statement on Whether Partial User Interface Used in Preparing Cryptocurrency Securities Transactions May Require Broker-Dealer Registration."

The statement indicates that, under the premise where transactions are entirely initiated and controlled by users, non-custodial service providers that offer neutral interfaces may not need to register as broker-dealers or exchanges.

Mixin is a decentralized, self-custodial privacy wallet designed to provide secure and efficient digital asset management services.

Its core capabilities include:

· Aggregation: integrating multi-chain assets and routing between different transaction paths to simplify user operations

· High liquidity access: connecting to various liquidity sources, including decentralized protocols and external markets

· Decentralization: achieving full user control over assets without relying on custodial intermediaries

· Privacy protection: safeguarding assets and data through MPC, CryptoNote, and end-to-end encrypted communication

Mixin has been in operation for over 8 years, supporting over 40 blockchains and more than 10,000 assets, with a global user base exceeding 10 million and an on-chain self-custodied asset scale of over $1 billion.

$600 million stolen in 20 days, ushering in the era of AI hackers in the crypto world

Vitalik's 2026 Hong Kong Web3 Summit Speech: Ethereum's Ultimate Vision as the "World Computer" and Future Roadmap

On the same day Aave introduced rsETH, why did Spark decide to exit?

Full Post-Mortem of the KelpDAO Incident: Why Did Aave, Which Was Not Compromised, End Up in Crisis Situation?

After a $290 million DeFi liquidation, is the security promise still there?

ZachXBT's post ignites RAVE nearing zero, what is the truth behind the insider control?

Vitalik 2026 Hong Kong Web3 Carnival Speech Transcript: We do not compete on speed; security and decentralization are the core

In-depth Analysis of RAVE Events: Short Squeeze, Crash, and Quantitative Financial Models of Liquidity Manipulation

Eve of Ceasefire, US Military Fires on Iranian Vessel | Rewire News Morning Brief

Figma's stock price drops over 7%, will Claude Design be the terminator?